Disclaimer

Figures are hypothetical and based on historical assumptions. They’re not guarantees and are for education only. A financial plan is an ongoing process that requires updates and judgment. Nothing here is individualized advice. If you’d like help pressure-testing your own plan, schedule a free intro call.

Video Overview

Background: Walter & Skylar

Walter and Skylar have two children, Walter Jr. and Holly. Walter, a highly educated former high-school chemistry teacher, shifted careers after a health scare and went on to run a successful pharmaceutical manufacturing and distribution venture before purchasing a car wash business. Skylar previously worked as a bookkeeper for Benecke Fabricators and now co-operates the car wash full-time.

They are within a few years of retirement and want clarity on:

- When they can retire

- What they can safely spend

- When to claim Social Security

- How to minimize taxes (including Roth conversions)

- How to leave a meaningful legacy

After researching planners, they narrowed their criteria to fee-only, fiduciary, and credentialed (CFP®) with relevant retirement experience. They scheduled a 30-minute intro call with Daniel at Masuda Lehrman Wealth...

Initial Consultation

In the intro meeting, Daniel asked focused questions to understand:

- What led them to seek advice now

- Their concerns and specific questions

- What a “win” looks like over the next 3-12 months

Following the call, Daniel sent a written proposal summarizing needs, scope, and fees.

Once they decided to proceed, Walter and Skylar e-signed the Client Agreement and onboarding began.

Daniel’s Financial Planning Process

Phase 1 — Gain Clarity & Get Organized (Month 1)

Walter and Skylar complete a concise financial questionnaire, upload documents, and connect their accounts to the planning tools. If they choose the AUM model, they also open and transfer accounts to Daniel’s custodian.

Phase 2 — Analysis & Recommendation (Month 2)

Daniel reviews, organizes, and analyzes their data and then hosts 60–90 minute Zoom sessions to iterate on the plan. Together, they answer:

- When can they retire?

- What can they safely spend?

- Which changes raise the odds of success?

Phase 3 — Refine & Implement (Month 3)

Daniel helps translate decisions into action, sets up monitoring systems, and schedules brief accountability check-ins (≤30 minutes).

___________________

Phase 1 in Detail: Gain Clarity & Get Organized

Clarifying Goals & Tradeoffs

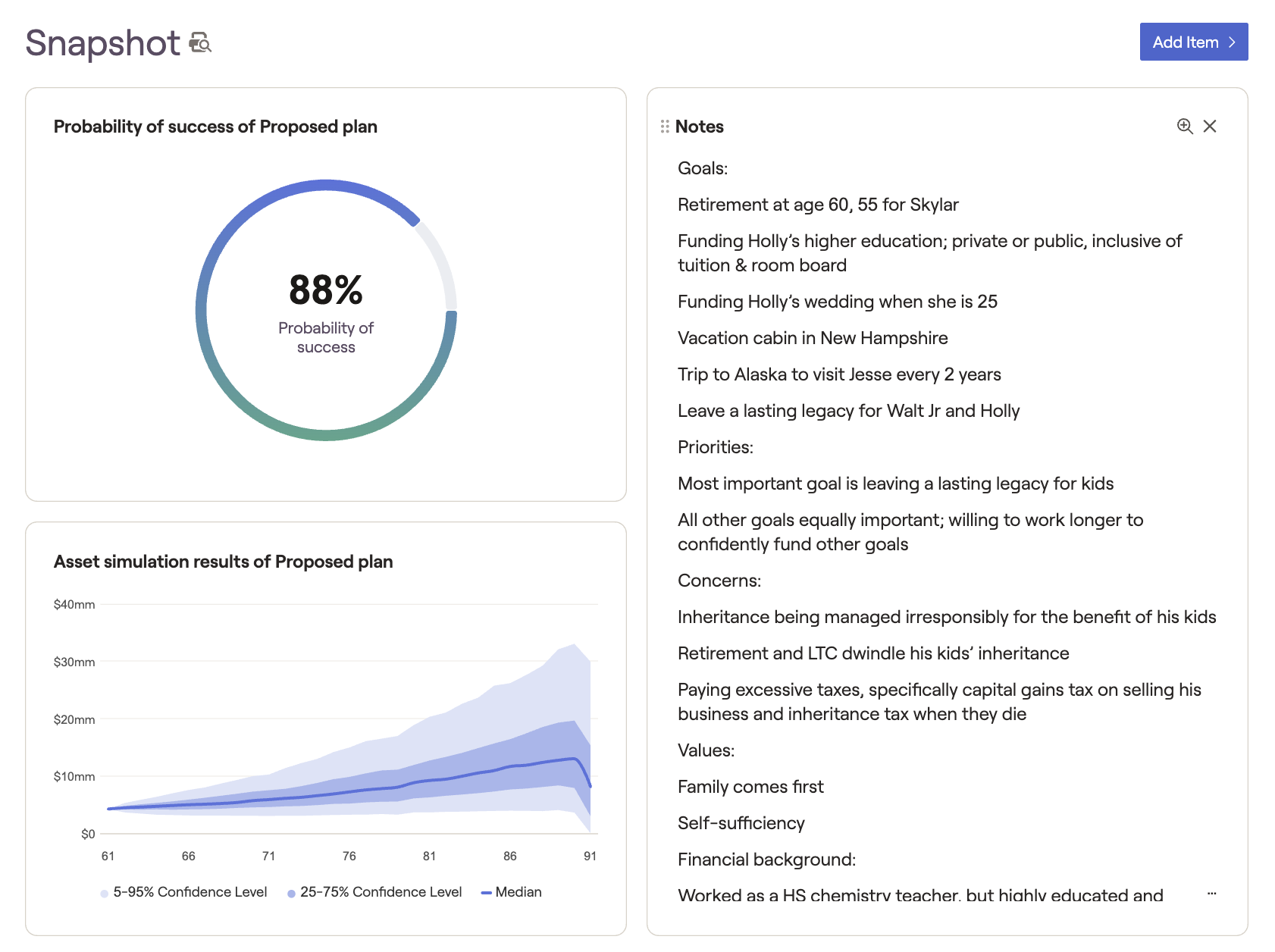

.png)

From structured conversations and a goals worksheet, Daniel captures the “why” behind the numbers:

- Retirement timing: Walter at ~67; Skylar at ~58

- Spending target: ~$7,500/month (before healthcare/LTC contingencies)

- Education: Fund higher education for Holly (tuition + room & board)

- Family & travel: Alaska trip every two years to visit a close friend

- Legacy: A high priority—Walter would like to leave ≥$5M to the children

- Business transition: Sell the car wash at retirement to simplify cash flow

They agree that legacy is “must-have,” while retirement date and spending can flex if needed.

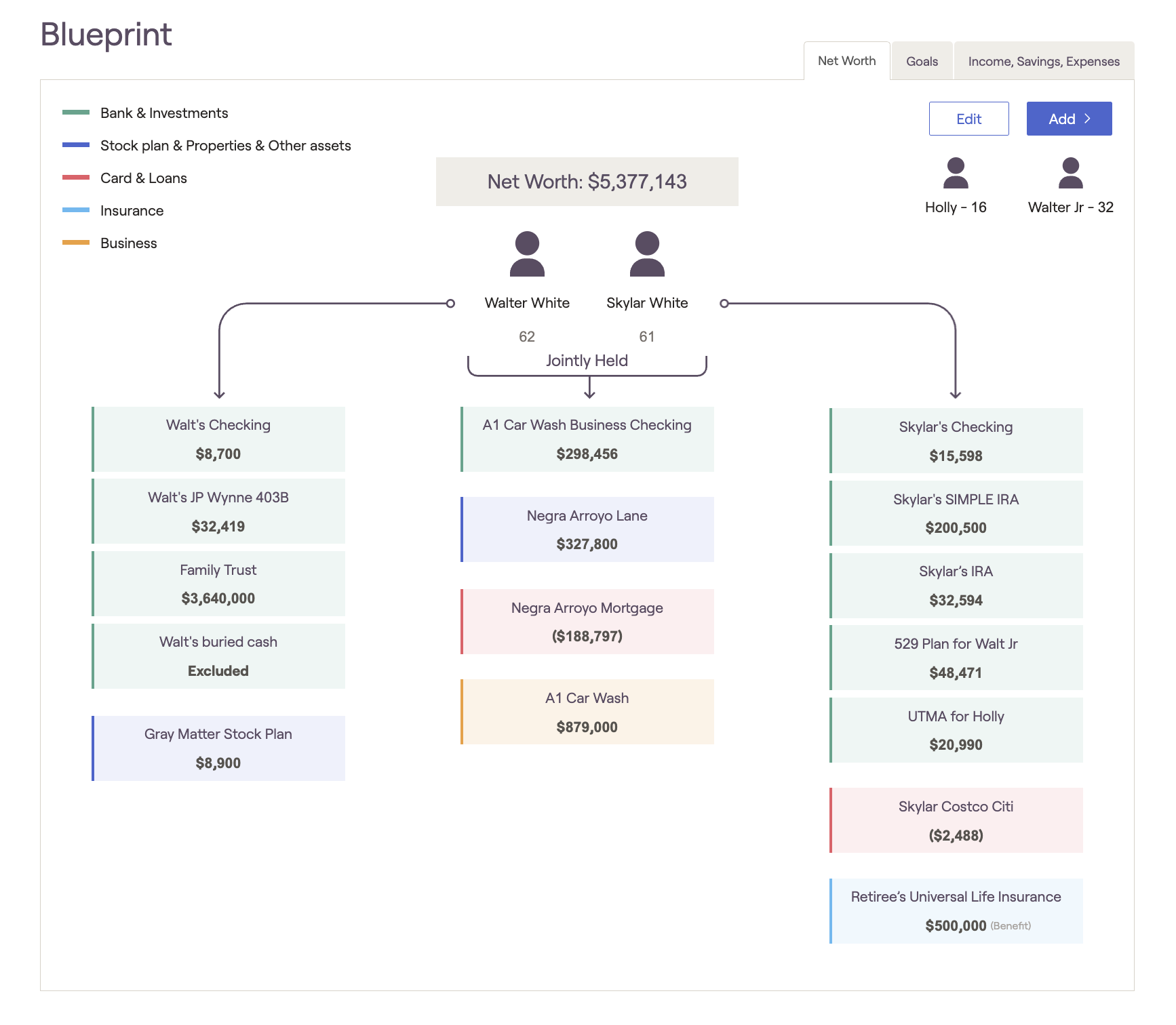

Gathering Documents

.png)

Walter and Skylar upload:

- Recent tax returns and W-2/1099s

- Statements for 401(k)/403(b)/457/TSP, IRAs, brokerage, bank, HSA

- Pension estimates and Social Security statements

- Insurance (life, disability, long-term care, annuities)

- Estate docs (will, trust, POAs, health directives)

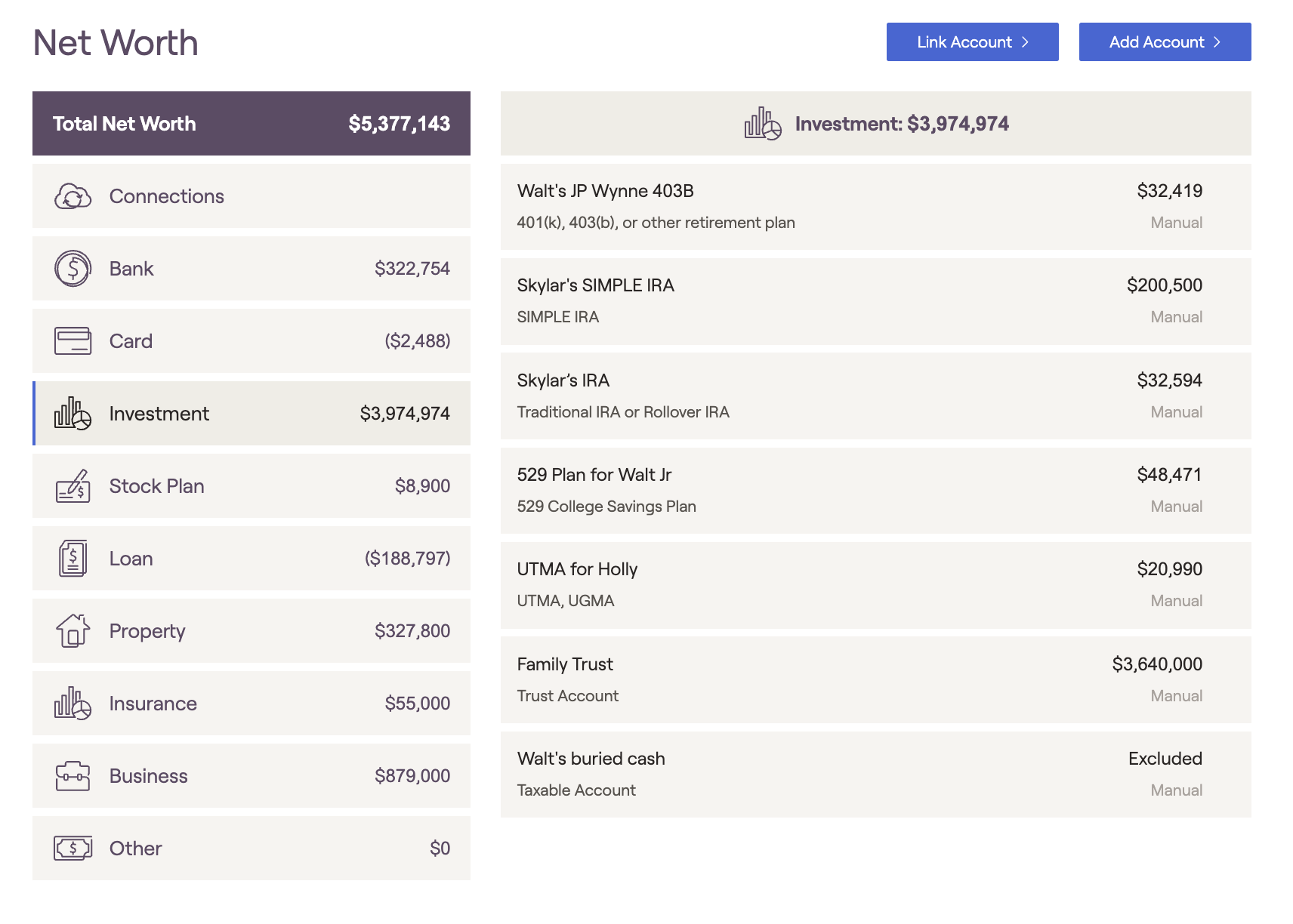

Setting Up Planning Tools

Phase 2 in Detail: The Analysis

With the discovery work complete, this phase turns insight into strategy. Daniel now takes the raw data—their income sources, investments, pensions, and expenses—and transforms it into a clear picture of where they stand and what’s possible. This is where financial planning shifts from numbers to decisions. Over the next several weeks, Daniel reviews, organizes, and analyzes every piece of information, then hosts a series of 60–90 minute Zoom sessions to refine the plan together. These meetings are highly interactive, designed to test real-life scenarios and explore tradeoffs so they can make confident, informed choices. Together, they’ll answer the questions that matter most:

- When can they retire?

- What can they safely spend?

- Which changes raise the odds of success?

Income: Timing, Sources, & Amounts

Daniel reviews the source, amount, and timing of all income streams—both before and after retirement—to anticipate tax implications and ensure smooth cash flow throughout the transition. The initial Social Security intent is for Walter to claim at 67 (FRA) and Skylar at 62, but Daniel flags this for review since timing affects lifetime income, survivor benefits, and overall tax efficiency. He explores the couple’s rationale and models alternative claiming strategies to help identify the optimal approach.

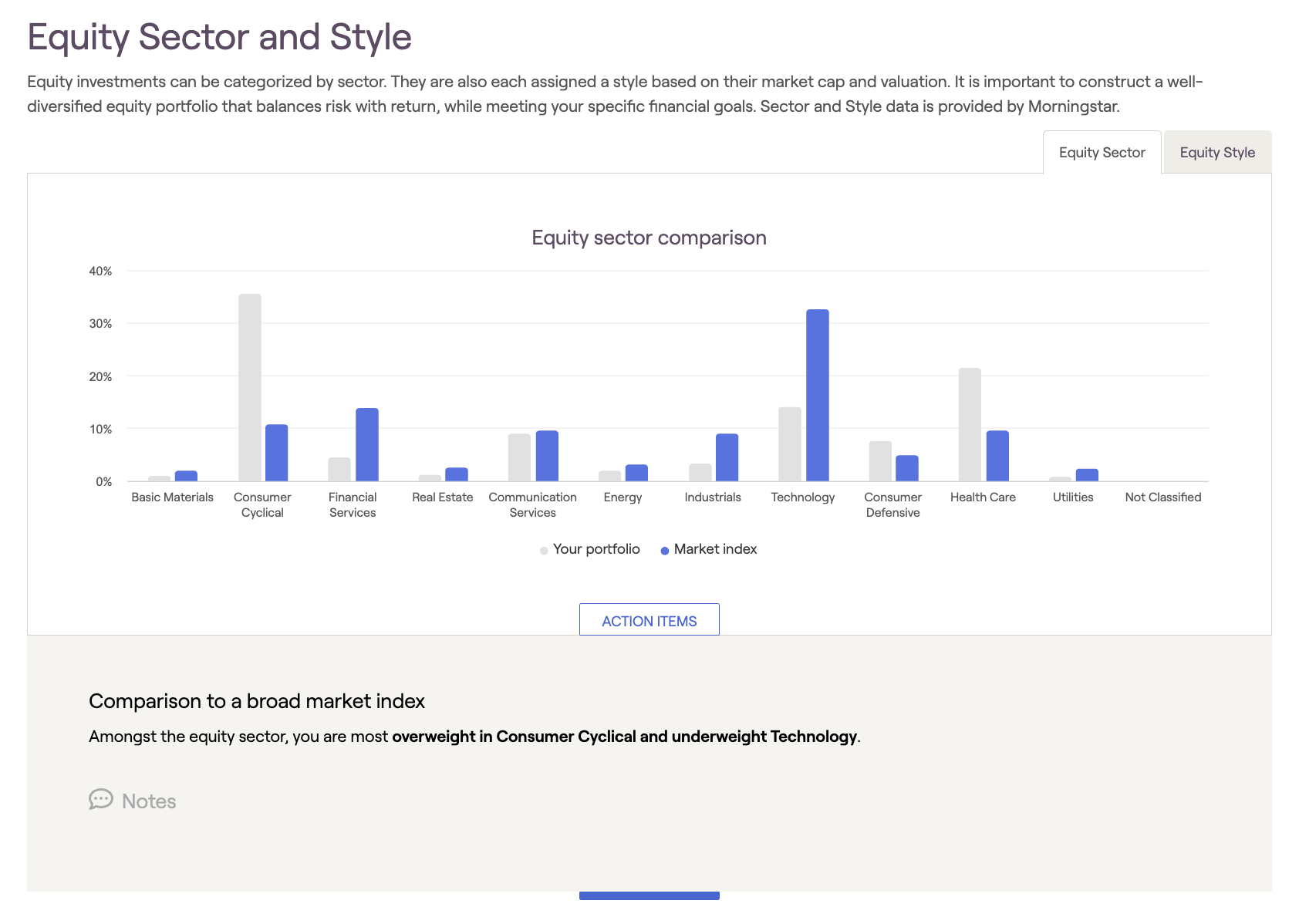

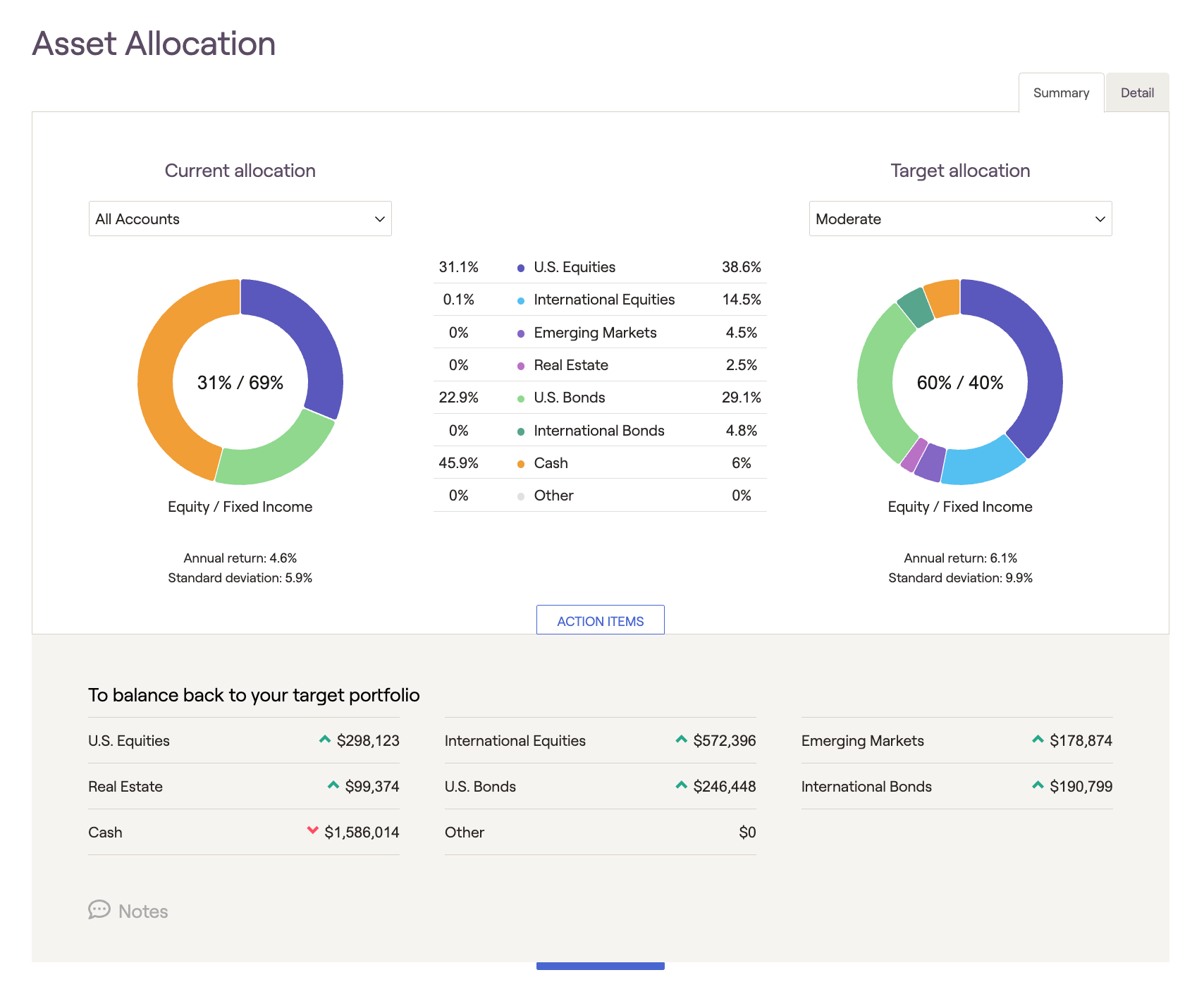

Portfolio & Allocation

Daniel first evaluates asset allocation (AA)—the primary driver of long-term outcomes. He notes excess cash (under-invested dollars) and asks about risk comfort and the reason for cash buildup.

He then reviews style/sector exposures relative to the broad market to check diversification. The current portfolio appears under-weighted to technology and over-weighted to consumer cyclicals versus the market—acceptable only if intentional; otherwise it introduces uncompensated tracking risk.

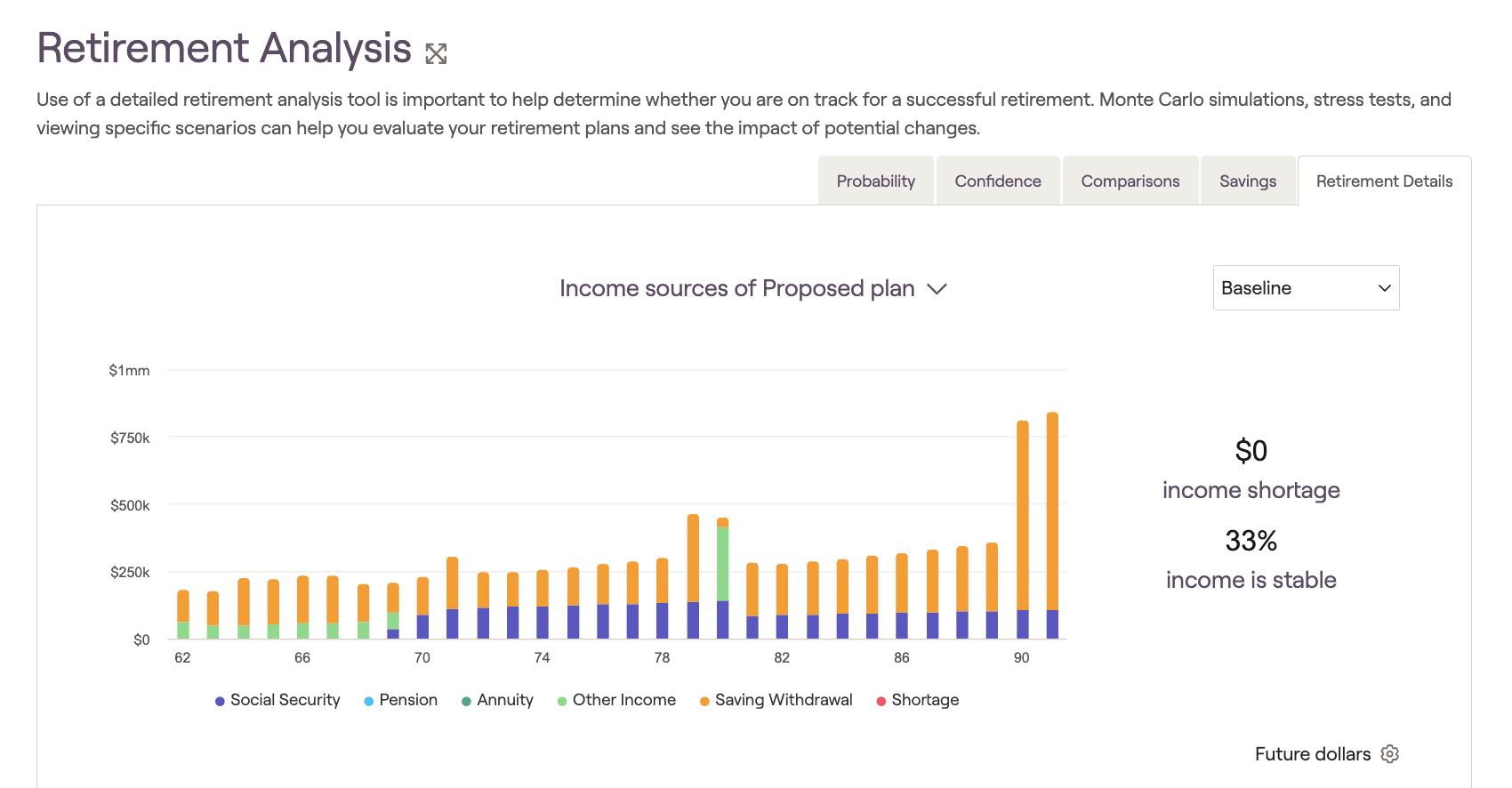

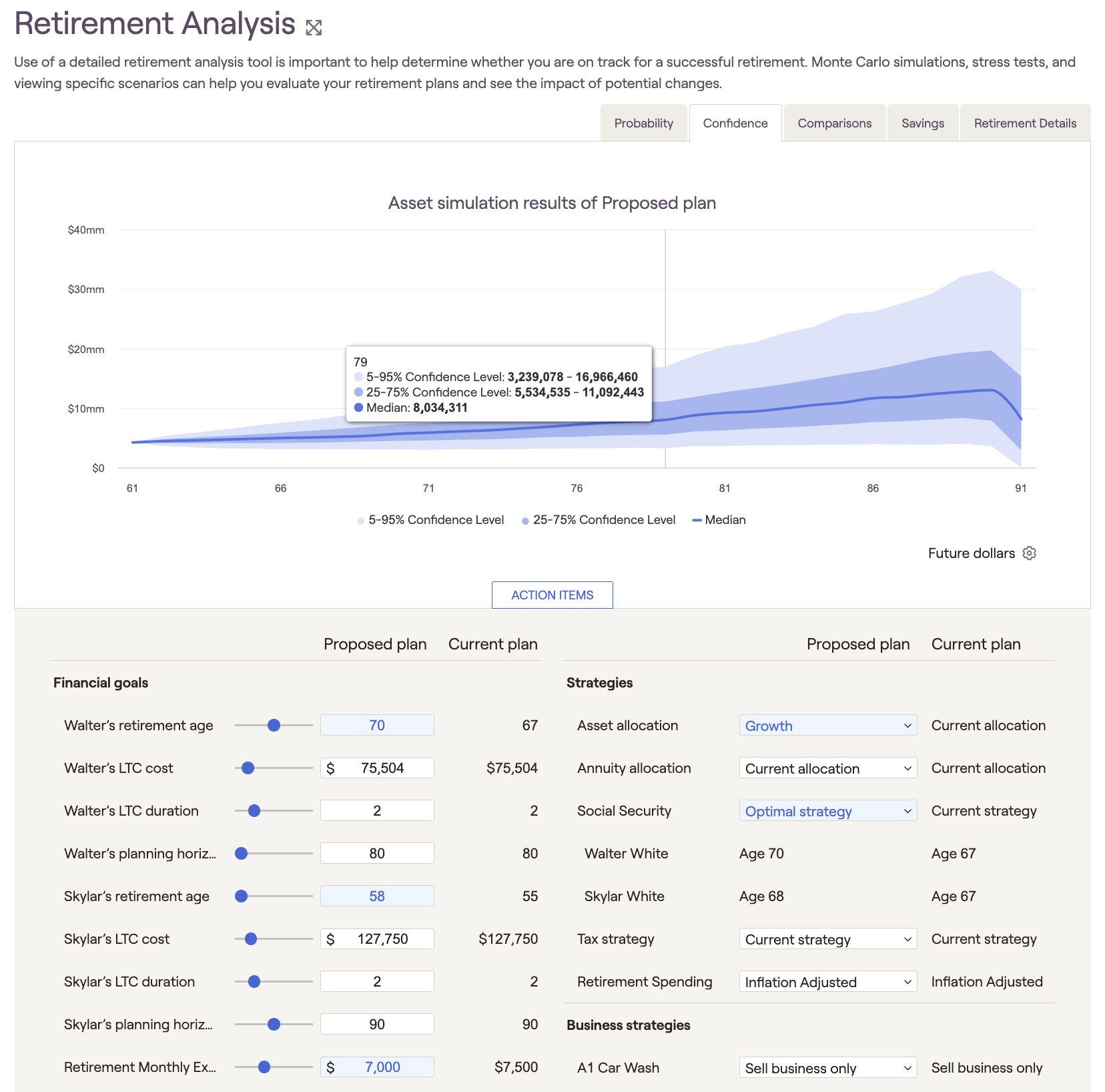

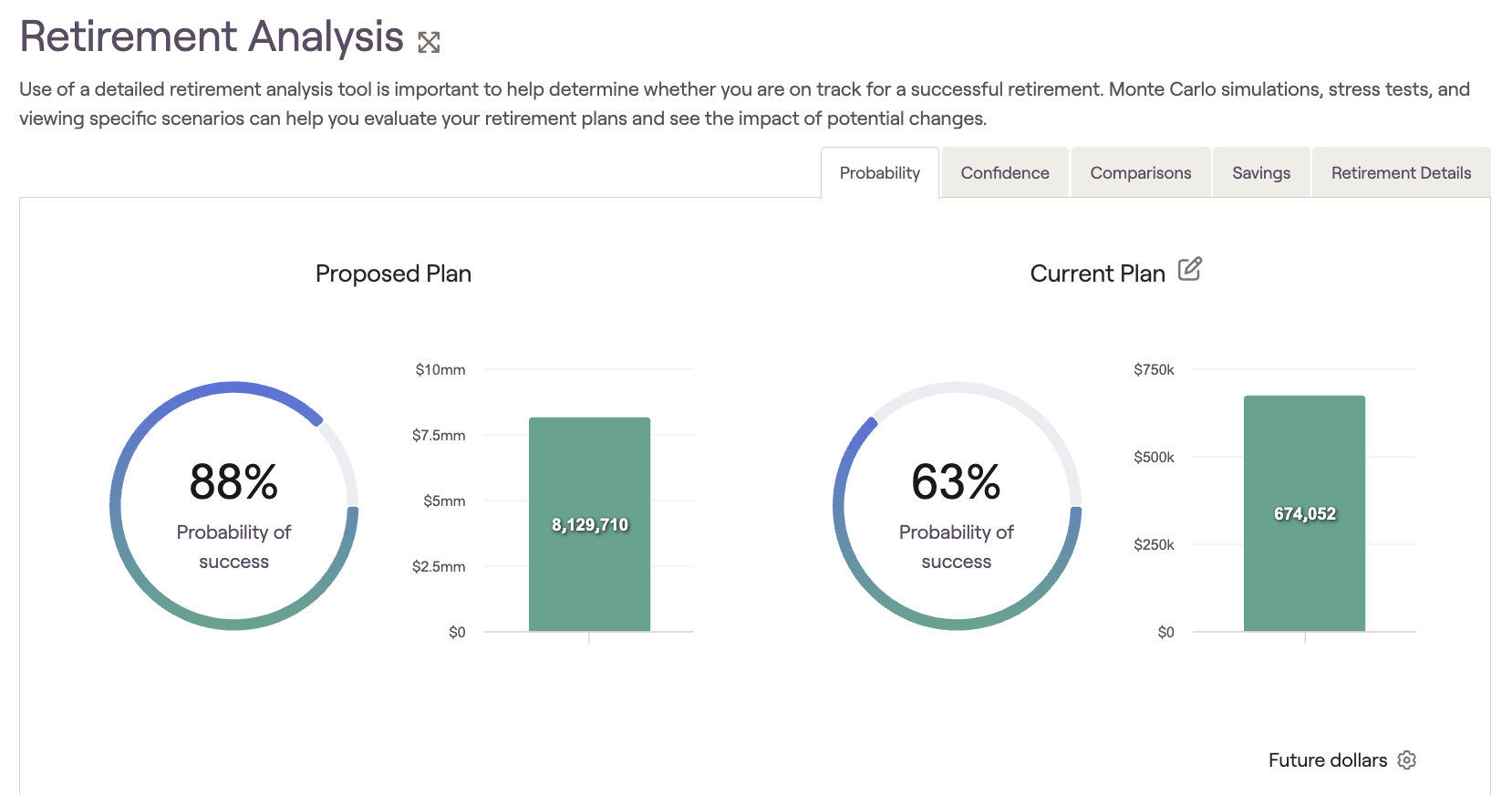

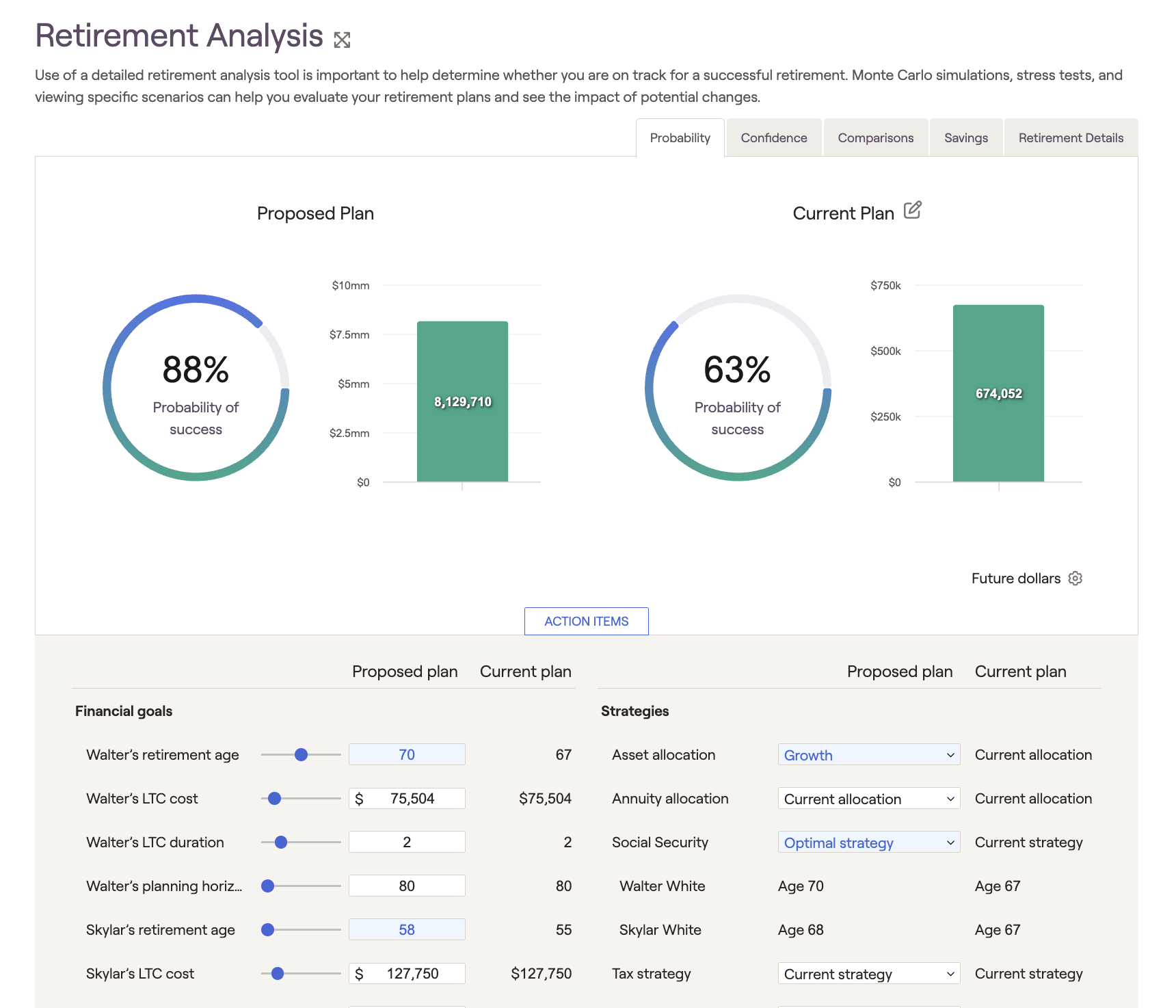

Retirement Readiness (Monte Carlo)

Daniel aggregates their goals, spending, income, and portfolio into a 1,000-trial Monte Carlo simulation.

This analysis models how their plan could perform across a wide range of market conditions—both good and bad. The result is displayed as a visual graph that starts as a narrow cone and gradually fans out over time. The widening shape represents uncertainty: in the early years of retirement, outcomes are relatively predictable, but as time passes, investment returns, inflation, and life events cause the range of possible results to spread wider. This visual helps them see not just whether their plan is likely to succeed, but also how sensitive it is to market volatility, spending choices, and timing decisions—turning abstract probabilities into a clear picture of long-term financial resilience.

Initial probability of success: ~63% (any score above 80% is considered a strong plan)

He uses this as a decision engine, testing levers (spend, work, save, allocation, Social Security timing, Roth conversions) and comparing scenarios side-by-side.

With a few modest changes—and one or two bigger levers—Walter & Skylar’s plan moves from the mid-60s to the high-80s probability of success. Daniel emphasizes the playbook and tradeoffs more than the single output number.

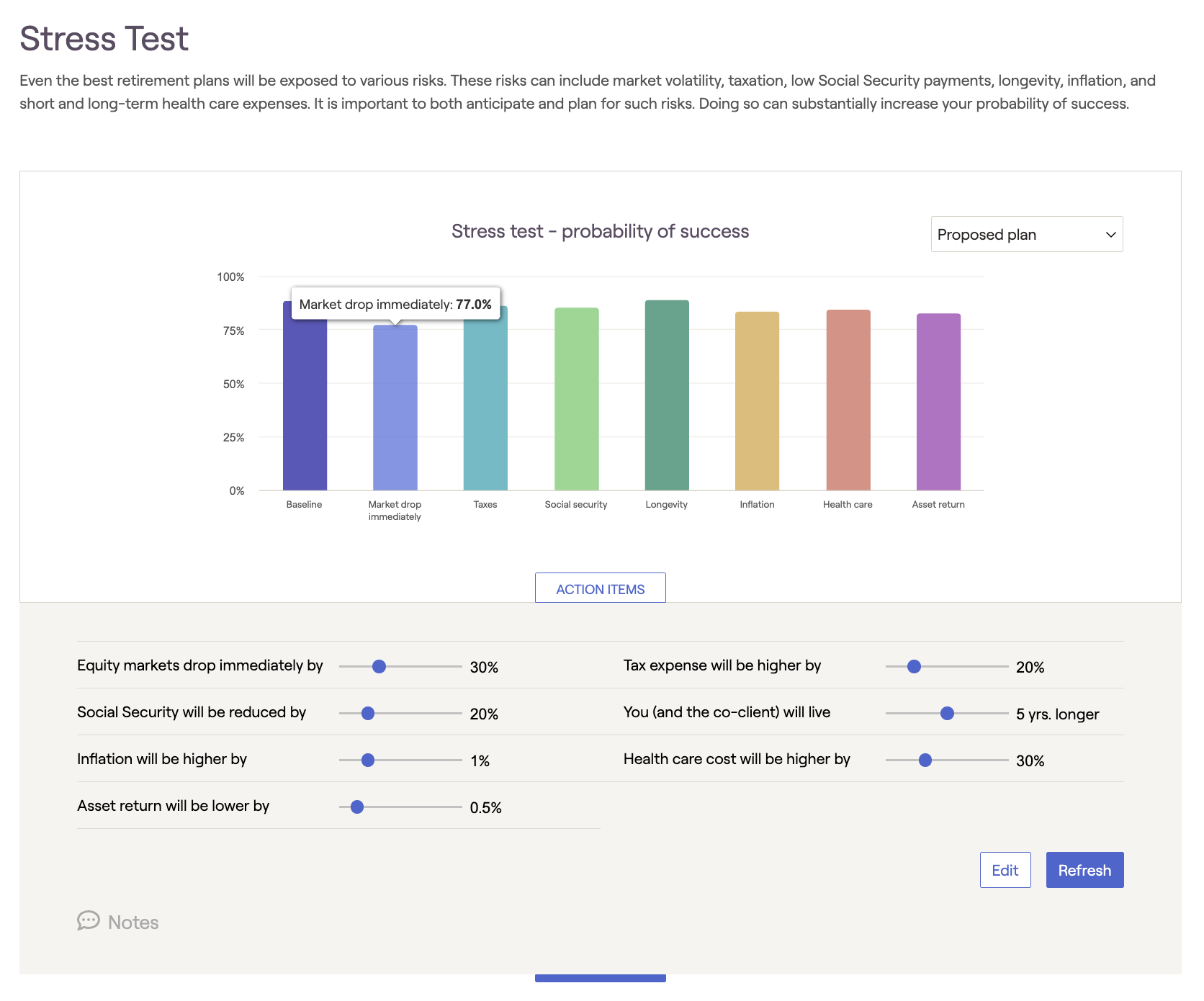

Daniel then stress tests to see how their plan holds up under adverse conditions—such as a major market downturn, higher inflation, or unexpected healthcare costs. By isolating and testing each scenario, he shows how these risks could affect their probability of success and long-term cash flow. This helps Walt and Skylar see which factors have the greatest impact and where adjustments—like reducing spending or shifting investment strategy—could strengthen their plan’s resilience.

Phase 2 in Detail: The Recommendation

With their Monte Carlo probability of success at 63%, Daniel identified several levers to improve Walter and Skylar’s plan while staying true to their goals and values. Since their top priority is leaving a $5M legacy, while retirement timing and spending are more flexible, the recommendations focused on optimizing income strategies, reducing idle cash, and considering modest lifestyle adjustments.

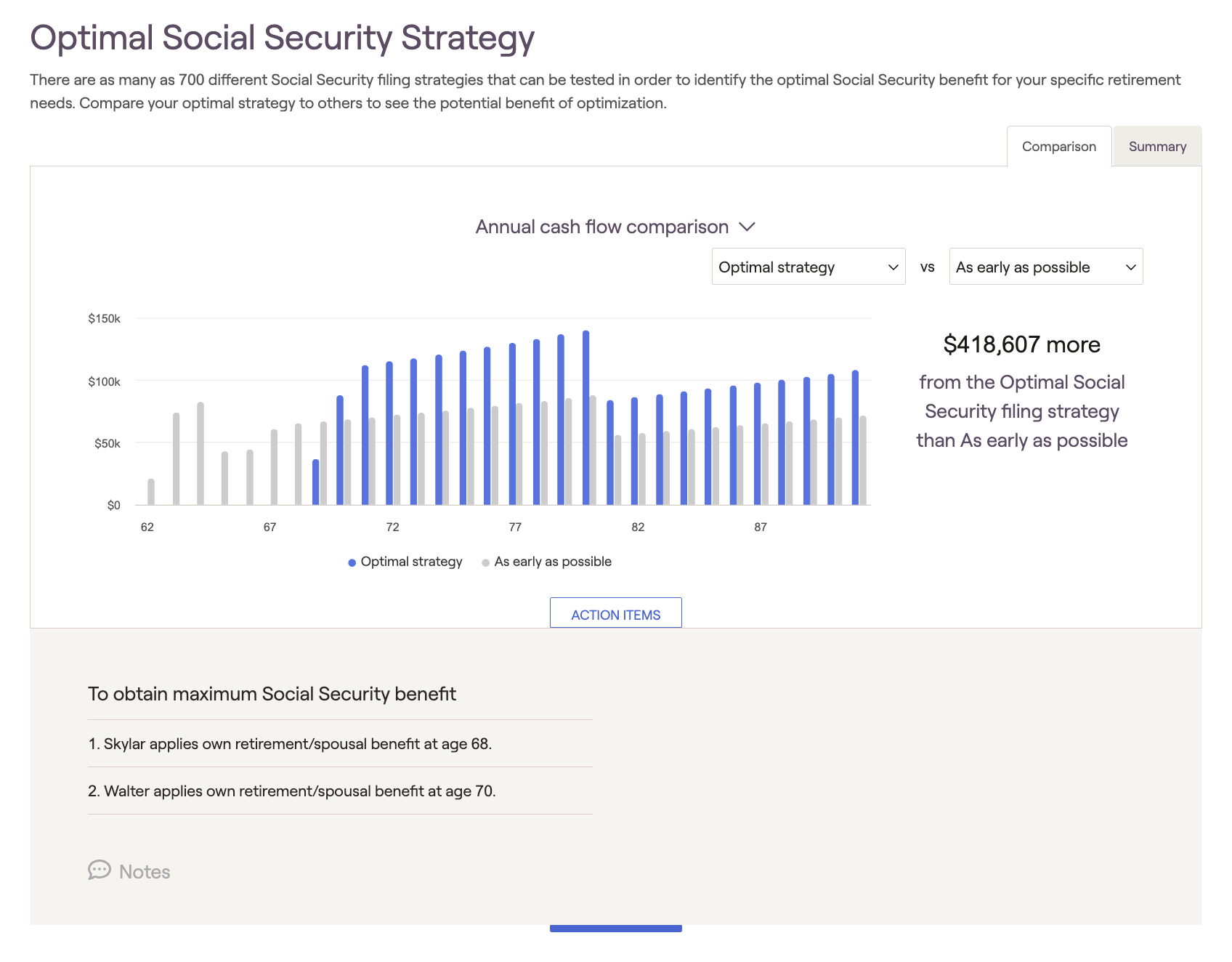

1) Optimize Social Security Strategy

Walter initially planned to claim at age 67 and Skylar at 62. Daniel modeled alternative strategies and recommended delaying Skylar’s claim until closer to age 68. This increases lifetime household income, strengthens survivor benefits, and meaningfully raises their retirement success probability without requiring additional savings.

2) Put Idle Cash to Work

A large portion of their portfolio was sitting in cash, which dragged on long-term growth potential. Daniel recommended investing these funds into a diversified, low-cost portfolio of stocks and bonds aligned with their risk tolerance and long-term legacy goals. Modeling showed that even a moderate reallocation improved their probability of success substantially.

3) Flex on Retirement Timing

While Walter and Skylar prefer to retire in about two years, they expressed openness to working longer if it meant greater confidence in funding goals. Daniel showed that delaying retirement by three years would add significant buffer: more years of income, fewer years of withdrawals, and additional growth in the portfolio.

4) Refine Cash Flow and Savings

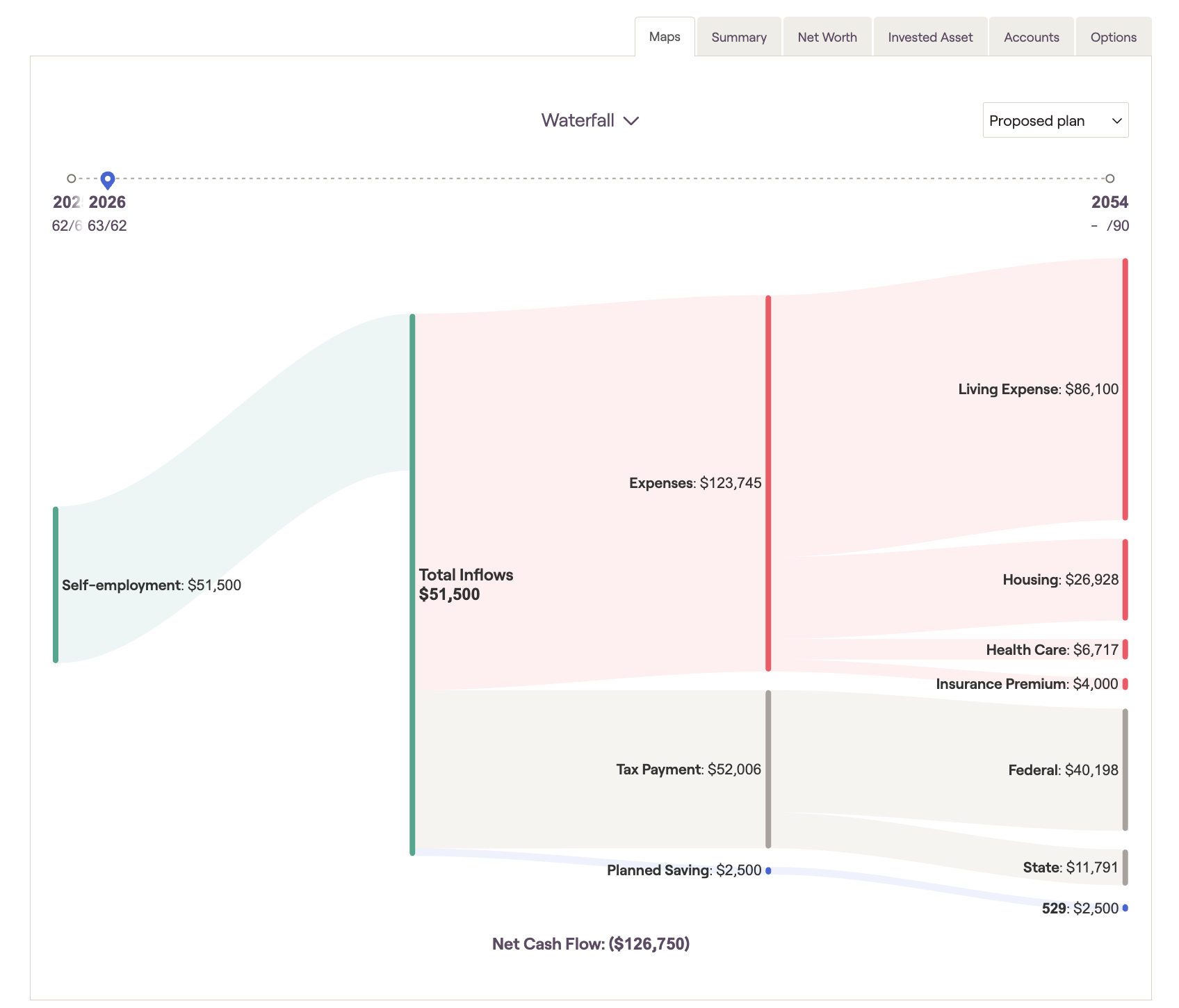

Cash Flow analysis provides Walt and Skylar with a clear, year-by-year view of how money moves through their plan. It shows their income from Social Security, portfolio withdrawals, and other sources alongside their spending, taxes, and savings, revealing each year’s net cash flow—whether they’re building reserves or drawing down assets. This helps them see how their income and expenses shift before and after retirement, ensuring they stay on track for long-term stability.

Phase 3 in Detail: Implementation

Clients receive concise status updates so they always know what’s finished and what’s next.

Daniel turns decisions into done:

- Project plan & deadlines with three short implementation check-ins

- Open/transfer accounts and automate contributions at Betterment for Advisors (or the client’s existing custodian, if preferred)

- Set rebalancing and tax-loss harvesting rules; update beneficiaries; coordinate with the CPA

- Execute Roth conversions and other tactics in the right years/amounts

Ongoing Relationship

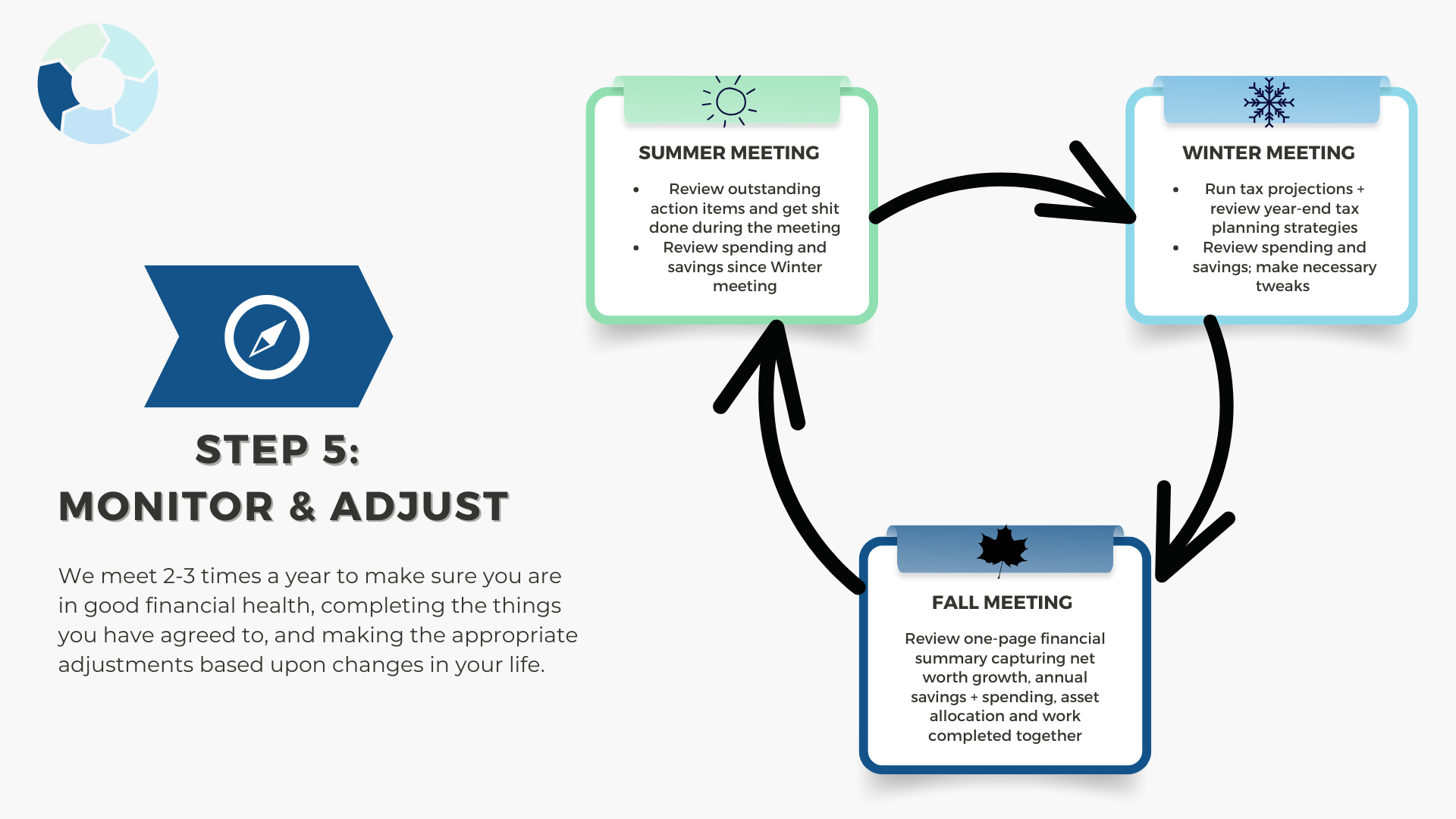

Daniel monitors, adjusts, and pivots as life unfolds:

- Markets, tax laws, family dynamics, health, values—all change; the plan should, too.

- Asset allocation: Rebalance and manage risk when thresholds or life events warrant.

- Spending: Track, review, and adapt withdrawal rates within guardrails.

- Cadence: Typically 2–3 meetings per year, plus ad-hoc access when life happens.

In Summary

This plan gives Walter and Skylar clarity about what’s possible, a simple playbook for what to do next, and a partner to keep it on track. We organized every moving part—income, investments, Social Security, taxes, and spending—into one picture, tested it against good and bad markets, and showed which small changes make the biggest difference. Instead of guessing, they now have clear answers to when they can retire, what they can safely spend, and how to improve their odds—plus ongoing monitoring so the plan adjusts as life changes. The result is less noise, more confidence, and a calmer path to the retirement they want.

Frequently Asked Questions

How long does the process take?

The initial planning sprint is typically 1–3 months, depending on complexity and scheduling.

What does it cost?

Daniel is fee-only. Most planning engagements use a transparent flat fee; ongoing management is optional under an AUM model. The exact fee is quoted up front.

Will a retirement plan actually help?

Yes. A good plan improves financial literacy, aligns money with values, and provides an adaptable playbook for both expected and unexpected events.

Ready to see your own plan with fresh clarity?

Schedule a free introductory call to explore next steps with Daniel.